Property Photography

The Building

Investment Opportunity — San Antonio, TX

22,170 SF · 100% NNN · S&P A+ Credit · I-35 Corridor

The Thesis

The market is pricing this asset at an 8.16% cap — 381 basis points above the 10-Year Treasury — because both leases expire December 31, 2028. That expiration risk is real, but it is materially overstated.

UnitedHealth Group operates this building as WellMed, their Optum subsidiary headquartered in San Antonio with 10,000+ local employees and 24% of Bexar County's commercial insurance market. They invested $1M renovating this building in 2025. A Sanitas Medical Center sublease is already embedded in Suite 501. The tenant has indicated renewal discussions can begin 24 months before expiration — January 2027.

When that renewal executes, the asset reprices from 8.16% to a stabilized 6.5% cap and sells to institutional buyers. You are buying a dollar of stabilized value for 73 cents.

Property Details

| Address | San Antonio, TX 78224 |

| Submarket | I-35 Corridor / SW Military Dr |

| Building Size | 22,170 SF |

| Suites | 14 individually metered |

| Occupancy | 100% |

| Tenant | UnitedHealth Group (WellMed / Optum) |

| Guarantor Credit | S&P A+ |

| Lease Type | Triple Net (NNN) |

| Lease Expiration | December 31, 2028 |

| 2025 Renovation | $1,000,000+ by tenant |

| Price / SF | $248/SF |

Property Photography

Financial Analysis

Income & Expense Statement

| Line Item | 2026 | 2027 | 2028 |

|---|---|---|---|

| Main Block Base Rent (17,196 SF) | $350,798 | $350,798 | $361,116 |

| Suite 101 Base Rent (4,974 SF) | $101,321 | $103,808 | $106,444 |

| Gross Base Rent | $452,119 | $454,606 | $467,560 |

| + NNN Reimbursements | $231,099 | $231,099 | $231,099 |

| − Reimbursable Expenses (wash) | ($231,099) | ($231,099) | ($231,099) |

| − Reserves ($0.15/SF) | ($3,325) | ($3,325) | ($3,325) |

| Net Operating Income | $448,794 | $451,281 | $464,235 |

Key Metrics at $5,500,000

| Purchase Price | $5,500,000 |

| Price Per SF | $248/SF |

| Going-In Cap Rate | 8.16% |

| Spread vs. 10-Yr Treasury | +381 bps |

| Year 1 NOI | $448,794 |

| NOI Growth (2026–2028) | +3.4% (contractual) |

| DSCR at 60% LTV | 1.60x |

| Stabilized Exit Value (6.5% cap) | $7,844,769 |

| Value Creation at Renewal | $2,344,769 |

Debt Service Coverage (60% LTV, 6.75%)

| Loan Amount | $3,300,000 |

| Annual Debt Service | $279,885 |

| Year 1 DSCR | 1.60x |

| NOI Cushion Above DS | $168,909 / yr |

| Break-Even Occupancy | 62.4% |

| Stress Test (NOI must fall) | 37.6% before DS uncovered |

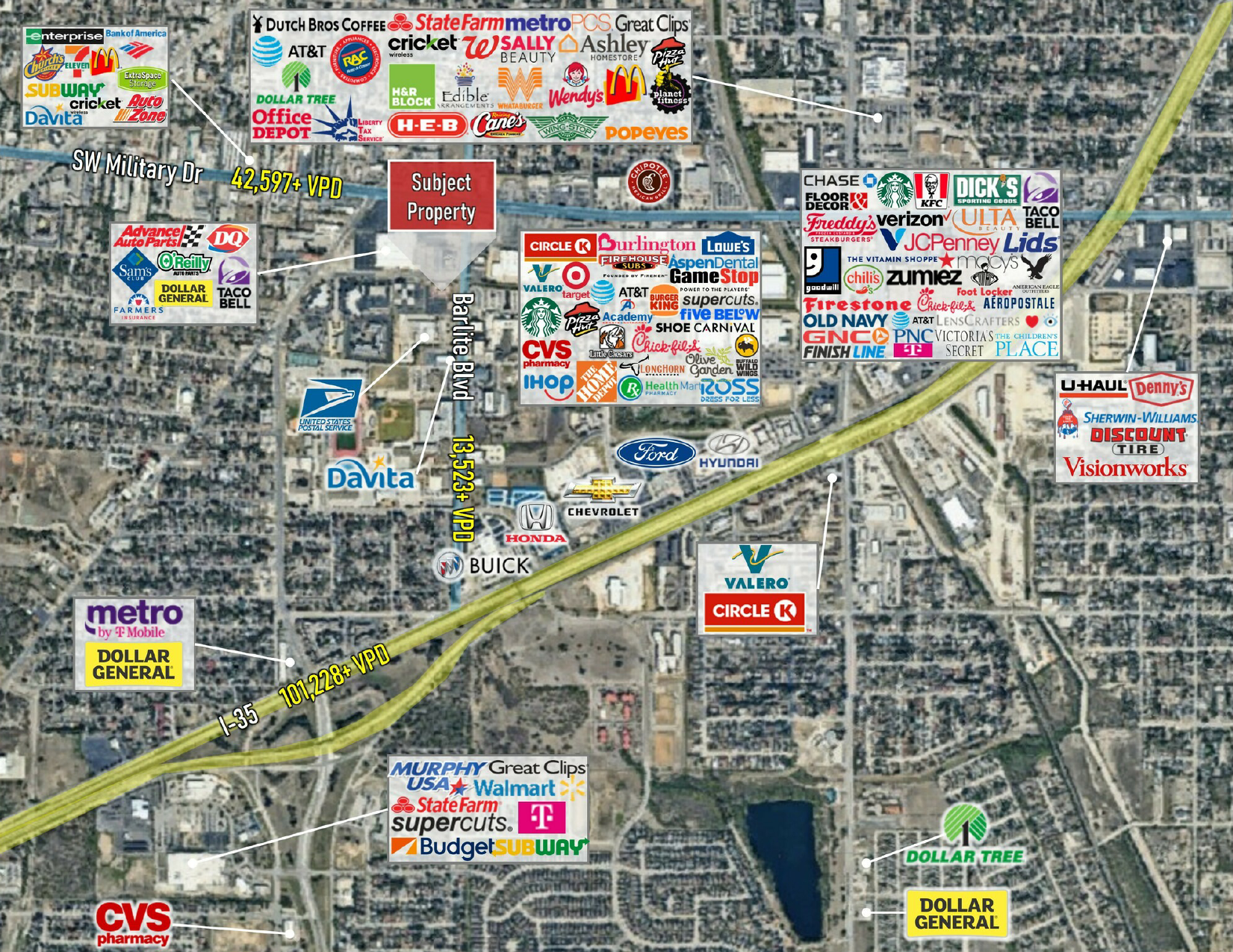

Location & Trade Area

The property sits at the intersection of I-35 (101,228 VPD) and SW Military Drive (42,597 VPD) — one of San Antonio's highest-traffic medical and retail corridors. The immediate trade area is anchored by Target, Home Depot, Sam's Club, Walmart, Chick-fil-A, and CVS within a half-mile radius.

San Antonio's medical office market is structurally undersupplied at the sub-10,000 SF suite level. Vacancy in the South San Antonio medical submarket sits at 6.2%, well below the metro average of 9.1%. Asking rents have increased 8.4% year-over-year. New supply is constrained by land costs and permitting timelines.

| Metric | Value |

|---|---|

| I-35 Traffic (VPD) | 101,228 |

| SW Military Dr Traffic (VPD) | 42,597 |

| 3-Mile Population | 98,400+ |

| Submarket Vacancy | 6.2% |

| YoY Rent Growth | +8.4% |

| WellMed SA Employees | 10,000+ |

| WellMed Bexar Co. Market Share | 24% |

Return Analysis

The probability-weighted gross profit across all scenarios is $2,761,391. The deal clears the $2M profit threshold in two of three scenarios on a levered basis, and in all three scenarios on an all-cash basis.

Probability-weighted gross profit: $2,761,391 · Probability-weighted IRR: 11.7% (all-cash) · All scenarios assume 6.5% exit cap on stabilized NOI.

Execution Plan

UHG has indicated renewal discussions can begin 24 months before lease expiration — January 2027, approximately 7 months post-close. The value creation event happens the moment the lease amendment is signed, not at sale. The asset reprices immediately upon execution.

UHG's cost to vacate and relocate is estimated at $40–60/SF ($887K–$1.33M) — furniture, medical equipment, IT infrastructure, patient notification, and revenue disruption. Against that switching cost, a modest TI allowance removes virtually all friction from the renewal conversation.

Risk Assessment

Aerial Views

Next Steps

The complete Offering Memorandum includes the full rent roll, lease abstract, financial waterfall, debt service analysis, and all three scenario models. Reach out directly — we respond to every inquiry personally.

We respond to every inquiry personally.